Imagine Russia as a combustion engine. Oil and gas pumped from its vast territories wash through the economy as taxes, government spending and investment. Foreign currency from oil and gas sales is used to fund imported equipment and products on shop shelves. Cash from the energy industry flows through companies and into pay packets. Whether directly or indirectly, Russians have oil money in their pockets.

So while on the face of it, the energy industry accounts for only around one-quarter of Russian output, in reality it is the source of up to 70 percent of Russia's gross domestic product, according to research by Andrei Movchan, an associate at the Carnegie Center in Moscow.

That helps explain how, in the late 1980s, a halving in the price of oil precipitated the collapse of the Soviet Union.

The current shock engulfing Russia is even more serious, Deputy Finance Minister Maxim Oreshkin told a conference hosted by Vedomosti, a business newspaper, in December.

Russia's isolation from the world economy due to sanctions imposed over Moscow's actions in Ukraine last year have worsened the impact of an oil price crash.

The Moscow Times looked at eight aspects of the crisis.

Oil

If the oil price falls to $50 per barrel it would cost Russia some $160 billion in lost annual exports, Oreshkin said. By mid-December, the price of oil had fallen not to $50, but to less than $40, following a collapse of the market last year amid chronic global oversupply.

Russia's response was to maximize output, raising oil production to its highest since the end of the Soviet Union and ramping up exports of gas and metals, prices of which have also fallen sharply.

This strategy has brought in extra money and preserved jobs, helping the country weather an economic contraction of around 4 percent this year. But it also undermined the future development of Russia's oil industry.

To maintain production volumes, oil companies are tapping easy-to-reach resources and neglecting investment in deposits that are harder to access, said Mikhail Krutikhin, a partner at consultants RusEnergy.

In the longer run, Russian oil output — which currently rivals Saudi Arabia at more than 10 million barrels per day — will decline sharply.

Sanctions

One of the reasons for the long-term decline in oil production is ongoing Western sanctions. Imposed last year, sanctions have deprived the oil industry of technology and expertise and sharply curbed lending by Western financial institutions to Russia.

This has forced Russian companies and banks to repay loans to foreigners rather than refinance them. Corporate external debt will drop to less than $500 billion by the end of the year from $660 billion in mid-2014, according to the Central Bank — the equivalent of sending around 9 percent of Russia's 2014 GDP over the border.

In the long run, reducing debt will leave Russia's finances in better health, said Chris Weafer, a senior partner at Moscow-based consultancy Macro Advisory.

But, he added, it is "a very narrow silver lining wrapped around a very dark cloud."

The Ruble

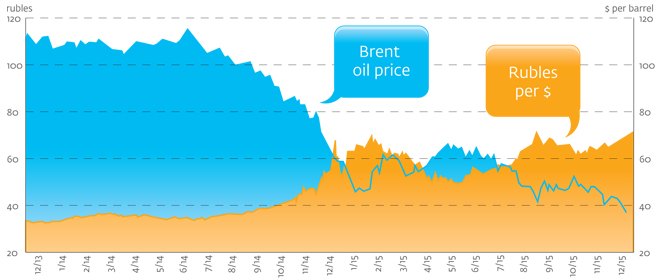

Russia has been able to cope with lower oil prices and sanctions by allowing the market to massively devalue the ruble, which has lost half its value against the U.S. dollar since summer 2014, when oil prices began to fall.

Non-interference in the ruble rate enabled the Central Bank to preserve its foreign currency reserves, which were at $371 billion in early December, rather than spend them to defend the currency.

Also, since oil and other commodities are sold in dollars, energy companies and the government earned more rubles for every dollar's worth of oil sold, offsetting the effect of the price fall and allowing the government to run a deficit of around 3 percent without borrowing or massive cuts to spending.

The weak ruble transformed Russia's trade balance, since anything brought from outside the country suddenly became far more expensive. According to official customs data, the value of imports fell by 38 percent in the first 10 months of the year.

This was another boon to the state, creating an expected current account surplus of more than $60 billion this year to help balance capital outflows and repayments to foreign creditors.

Other side effects of the devaluation were less positive.

Inflation

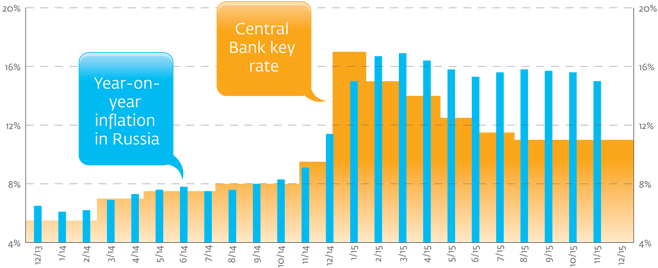

The ruble's collapse has caused prices to spiral. Inflation remained above 15 percent throughout 2015. Food prices rose even faster, as a consequence of bans imposed by Moscow on produce from the U.S., European Union and some other countries in retaliation to sanctions.

Inflation far exceeded wage growth, and real incomes began to fall at levels unprecedented since the 1990s. Household spending dropped by around 9 percent, according to the Central Bank, undermining a key driver of economic growth.

Meanwhile, 2.3 million more people fell into poverty in the first 9 months of the year, according to the Rosstat state statistics service. The creation of a middle class — a key development of President Vladimir Putin's reign — stalled.

Interest Rates

To keep inflation in check, the Central Bank kept interest rates high. Following an emergency hike to 17 percent last year, the bank's key rate has fallen to 11 percent.

This has raised borrowing costs and dampened investment. Already in short supply as oil wealth and foreign credit dried up, investment has fallen by around 5.5 percent in the first 10 months of the year, according to Rosstat.

High lending rates have come on top of Russia's old problems of corruption, red tape and rapacious officials — none of which have been effectively reformed. In an interview in October on state television's Channel One, Economic Development Minister Alexei Ulyukayev said there was no investment because there was no trust in Russian institutions or the country's future.

"Right now," he said, "you have to be a brave, even crazily brave person to open a business."

Import Replacement

The weak ruble should have boosted local production to replace more expensive foreign goods.

One industry that did expand was agriculture, where import bans and government calls for self-sufficiency for national security reasons gave extra impetus to ramp up production.

As other sectors of the economy shrank, "agriculture is demonstrating positive dynamics, with an at least 3 percent growth," Putin said at a press conference in December.

But the speed of change and the lack of competition have often come at the cost of quality. Many local products now on sale are substandard, and the dairy industry is rife with cheap palm oil supplements.

With Turkey and Ukraine recently added to the list of countries whose products have been banned, Russia could face food shortfalls of fruits and vegetables next year, the Central Bank warned in a December report.

Unemployment

Despite the recession, unemployment has stayed low, at around 5.5 percent. Companies and government bodies have preserved jobs by cutting pay and hours. Migrant workers, who are easier to fire and whose remittances have shrunk as the ruble has weakened, have left in droves, reducing the supply of labor.

Between January and early December, the number of Tajik citizens in Russia fell by around 100,000, or 10 percent, and the number of Uzbeks declined by more than 330,000, or 15 percent, according to Federal Migration Service data.

These factors have acted as a shock absorber for the labor market. "In another country unemployment would be in double digits," said Weafer.

Discontent?

Putin's support remains high. State television, through which most Russians get their news, has convinced the public that external factors, or anti-Russian conspiracies, are behind the economic slump.

But people are increasingly feeling the crisis. A survey by state pollster VTsIOM in December found that people's assessment of their wealth fell sharply at the end of the year. A quarter of respondents said their family finances were in a bad state.

In late 2014, Putin said oil prices under $80 would "destroy the global economy."

Both the global and the Russian economy have proven more resilient. But if oil prices stay low, the recession will continue throughout next year and an extended investment slump will stunt Russia's long term growth prospects.

Russia will enter its longest period of falling incomes and quality of life since the economic crisis that doomed the Soviet Union. Ahead of presidential elections in 2018, poverty, which more than halved during Putin's first 13 years in power, will be back with a vengeance.

Contact the author at [email protected]

A Message from The Moscow Times:

Dear readers,

We are facing unprecedented challenges. Russia's Prosecutor General's Office has designated The Moscow Times as an "undesirable" organization, criminalizing our work and putting our staff at risk of prosecution. This follows our earlier unjust labeling as a "foreign agent."

These actions are direct attempts to silence independent journalism in Russia. The authorities claim our work "discredits the decisions of the Russian leadership." We see things differently: we strive to provide accurate, unbiased reporting on Russia.

We, the journalists of The Moscow Times, refuse to be silenced. But to continue our work, we need your help.

Your support, no matter how small, makes a world of difference. If you can, please support us monthly starting from just $2. It's quick to set up, and every contribution makes a significant impact.

By supporting The Moscow Times, you're defending open, independent journalism in the face of repression. Thank you for standing with us.

Remind me later.